The coronavirus pandemic has delivered the biggest global economic meltdown since the 2008 financial crisis, which sparked the genesis of blockchain and cryptocurrencies.

Will virtual assets survive COVID-19? From Abu Dhabi to Zimbabwe, these 7 countries’ recent regulatory reforms on 4 continents say yes.

Table of Contents

- Abu Dhabi (UAE): FSRA virtual asset policy fits FATF R.16 travel rule

- South Korea: Act legalizes crypto with FATF’s “travel rule”

- Germany: BaFin decrees Bitcoin a legal financial instrument

- India: Supreme Court reverses Reserve Bank’s crypto ban

- France: Court rules Bitcoin should be treated as money

- United States: Updated Crypto-Currency Act of 2020 proposed

- Zimbabwe: Reserve Bank develops a regulatory sandbox for crypto

The worldwide coronavirus pandemic has caused pandemonium in both traditional and cryptocurrency markets since 13 March 2020, despite several big regulatory wins for cryptocurrency so far this year.

With no end to this financial and humanitarian crisis in sight, we feel it’s important to revisit these recent reforms as an antidote to the current dystopian doom-and-gloom.

From Abu Dhabi’s simplified crypto regulations to Zimbabwe’s regulatory sandbox for crypto companies to help micro-financing, these 7 countries’ regulatory reforms indicate that virtual assets will survive the COVID-19 pandemic.

TL;DR Summary

- Abu Dhabi (UAE) has simplified its regulatory approach to crypto

- U.S. draft bill matches digital asset types with specific regulators

- Korea’s amended law has legalized crypto ownership and trading

- Germany’s main regulator has classified virtual assets as financial instruments

- India’s top court gave exchanges access to banking services again

- In France, a court decision has made Bitcoin legal tender

- Zimbabwe’s regulatory crypto sandbox will help micro-financing

1. Abu Dhabi (UAE): FSRA aligns virtual asset policy with FATF R.16

Abu Dhabi Global Market (ADGM)’s Financial Services Regulator Authority (FSRA) has amended its virtual asset legislation on February 28 to align its AML/CFT policy with the FATF Standards’ latest updates.

The ADGM financial center published a report on the FSRA’s changes, such as rewording “crypto-assets” to “virtual assets” in line with FATF’s official terminology.

The ADGM also introduced other new regulations that create easier-to-understand rules for crypto companies to follow, such as moving crypto regulations from the narrow “Operating a Crypto Asset Business” category to the broader “Regulated Activities” category.

These latest FATF-facing regulatory reforms come in the wake of the UAE’s successful mutual evaluation at the FATF’s February plenary, where member countries were implored to implement the Recommendation 16 travel rule by the end of June 2020.

2. South Korea: Act legalizes crypto and enforces FATF’s “travel rule”

During a special plenary meeting on 5 March 2020, South Korea’s national assembly voted in favor of an amendment to their Financial Services law that essentially legalizes the ownership and trading of cryptocurrencies in the crypto-embracing nation and lays a solid foundation on which to build on.

Importantly, Korean regulators have now taken control of the largely unregulated crypto exchange scene.

Korea’s new legislation requires all virtual asset service providers (VASPs, a term adopted from the Financial Action Task Force’s Recommendation 16 update in June 2019) to:

- open a real-name bank account with an authorized Korean bank

- register it with Korea’s Financial Intelligence Unit (FIU)

- integrate a technical solution to comply with the FATF’s R.16 “travel rule” requirements

- If successful, apply for an ISMS certificate

Most of the regulations have been in place since 2018, but have been only been implemented by the biggest 4-6 exchanges until now, as Korean banks have been notoriously anti-crypto due to the systemic money laundering and security risks present in the country’s virtual asset industry.

Why it’s important

The updated Act brings legal certainty and clear rules for crypto investors and exchanges in Korea, one of the earliest and most fervent mass adopters of digital assets. Hopefully, the new Act will help to drive out bad actors, provide better legal protection for users and attract new institutional investments.

3. Germany: BaFin decrees Bitcoin a legal financial instrument

Following in the wake of the 5th Anti-Money Laundering Directive (AMLD5)’s January 10th transposition deadline and with only months to go before the FATF’s Recommendation 16 implementation review, European nations like Germany are starting to get their house in order.

BaFin, Germany’s Federal Financial Supervisory Authority (Bundesanstalt fur Finanzdienstleistungsaufsicht) announced a new guidance that surfaced on March 2, 2020.

The guidance essentially legalizes and positions both cryptocurrencies and crypto service providers within the current framework of Germany’s legal system.

BaFin drew up its new regulations in accordance with global AML/CFT measures to deal with cryptocurrencies, such as the FATF’s R.16 travel rule.

In December 2019, Bafin used the German Banking Act (Kreditwesengesetz or KWG) in line with the 5th Anti-Money Laundering Directive (AMLD5) to define both virtual assets as well as custodial service businesses.

BaFin now considers a crypto custodian business as an entity that manages and protects digital assets or associated private keys that can be used to move said assets to others as a financial service.

This definition came into effect on January 1st, 2020 and has made it a more straightforward process for German banks to compliantly start offering crypto-related financial services in 2020.

BaFin’s guidance defines cryptocurrencies as a “digital representation of value” not created or underwritten by a central bank or public institution and which therefore does not enjoy the legal status of fiat currency or money. However, virtual assets can constitute an agreement for or fulfillment of an investment or payment which can be received and digitally transferred, stored or traded.

Any company that wants to offer crypto-related services in Germany must now express their intent to do so by the end of March 2020 and apply for a BaFin financial license before December 2020. Applications will be reviewed case-by-case. Over 40 financial institutions have so far registered their intent to offer crypto-related services in Germany.

On 26 February BaFin showed it meant business regarding the enforcing of its new legislation, by closing down the Berlin-based crypto company KK UTG for advertising and selling Bitcoin ATMs. The regulator later contended that virtual assets are financial instruments as per the country’s banking act and that KK UTG does not have the required licensing or regulatory approval to conduct business in Germany.

Why it’s important

Following this guidance, Germany’s regulators now broadly view cryptocurrencies as legal financial instruments and crypto service providers (VASPs) who facilitate the exchange of virtual assets for fiat currency (or vice versa), as legal financial service institutions.

From this it follows that both VASPs and virtual assets are now subject to Germany’s banking and financial regulations and that traditional financial institutions can start to consider cryptocurrency-related services for their customers.

4. India: Supreme Court reverses Reserve Bank’s crypto ban

In 2018 the Reserve Bank of India (RBI) shocked the crypto world (and helped crash the price of cryptocurrencies) when it banned banks from working with crypto-dealing companies.

On March 10th, 2020, India’s Supreme Court overturned the Reserve Bank’s ban in a detailed 180-page ruling that criticized its heavy-handed approach to crypto regulation, which could have even worsened money laundering and terrorist financing activities by forcing it underground, making it much harder to track.

Why it’s important

The RBI has launched an immediate appeal for a review, and might very well be successful with it. However, the lifting of the ban has allowed Indian cryptocurrency companies to once again start doing business, while the Indian government and regulators figure out their strategy to comply with the FATF’s AML/CFT measures.

5. France: Court rules Bitcoin must be treated as money

During a recent court case, the Commercial Court of Nanterre ruled on 26 February 2020 that Bitcoin should be treated as a currency. In a dispute between the French virtual asset exchange Paymium and investment company BitSpread, the court categorized as a fungible asset that can be interchanged but not individualized.

In 2014, Paymium transferred 1000 Bitcoin to BitSpread as a loan (current market value $7.8 million). In late 2017, the Bitcoin blockchain underwent a controversial hard fork which resulted in a 1:1 issuance of the new digital asset Bitcoin Cash (BCH) in an “airdrop” to all Bitcoin holders. This allowed BitSpread to gain possession of 1000 BCH, which reached an all-time high price of $4000 soon after. Currently, the 1000 Bitcoin Cash assets are worth around $300,000.

By legally classifying Bitcoin as a fungible asset, the court categorized the lending of it as a consumer loan, which as a result transferred ownership of the 1,000 BTC to BitSpread, the borrower, over the course of the loan.

Therefore, the court found the airdropped Bitcoin Cash should be viewed and treated similarly to traditional stock dividends.

Why it’s important:

According to French legal expert Hubert de Vauplane, the court’s decision is critical:

“The scope of this decision is considerable because it allows Bitcoin to be treated like money or other financial instruments. It will therefore facilitate Bitcoin transactions, such as lending or repo transactions, which are growing, and thus favor the liquidity of the cryptocurrency market.”

Why it’s important

By clarifying its regulatory approach towards virtual assets and also simplifying its existing framework, Abu Dhabi has taken the initiative in the United Arab Emirates and the Middle East on how to define and regulate virtual assets in line with the approach of global regulators like the FATF. This now makes regulatory compliance a more straightforward legal process that should boost crypto-driven activity in this wealthy region.

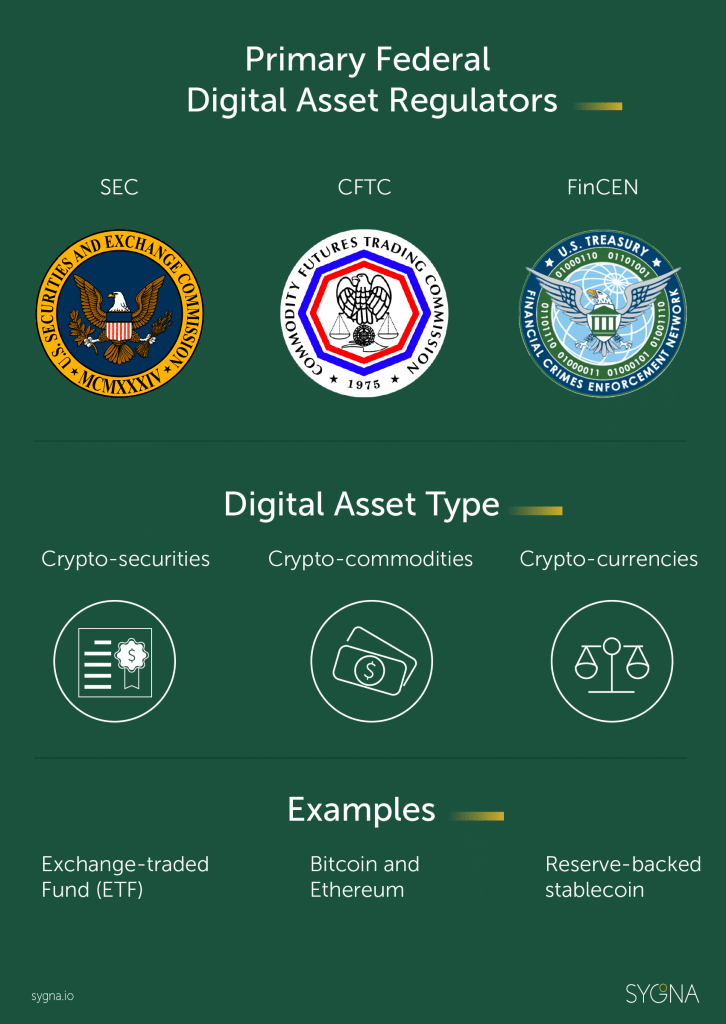

6. United States: Updated Crypto-Currency Act of 2020 goes to Congress

On 9 March, U.S. congressman Paul Gosar (Rep-Arizona) presented Congress with the latest updated draft proposal to help regulate digital assets in the United States by clearly defining different asset types, underlying technology, and regulators responsible for each asset class.

The latest version of the Crypto-Currency Act of 2020 has gone through dozens of iterations since December 2019. The March version includes new terminology such as “decentralized cryptographic ledger” and “smart contract” to help lawmakers understand the underlying technology, and also renames the “Federal Crypto Regulators” (FinCEN/SEC/CFTC) as “Primary Federal Digital Asset Regulators”.

Digital assets are split into the categories of:

- Crypto-commodity (ie. Bitcoin etc)

- Crypto-currency (a digital representation of the U.S. Dollar or other fiat currencies, thus including stablecoins like Tether, Gemini Dollar and other reserve-backed or synthetic stablecoins)

- Crypto securities.

For a full breakdown, read our detailed Crypto-Currency Act of 2020 guide here or click the image below.

Why it’s important

While the proposed crypto act has had a lukewarm reception and there’s a good chance it will not be pushed through, it certainly shines a welcome light on the lack of a clear overarching regulatory digital asset strategy in the U.S. and proffers a reasonably well-structured way forward.

7. Zimbabwe: New regulatory sandbox set to help crypto micro-financing

In middle March, good news came from Zimbabwe, the Southern African country that has been ravaged by political turmoil and hyperinflation over the last two decades.

With a new president and both political and economic reforms on the horizon, Zimbabwe is now trying to relaunch their Zim Dollar (with mixed results) and is also making a U-turn on their cryptocurrency policing.

Zimbabwean authorities have announced that it is busy developing a regulatory sandbox for cryptocurrencies that will establish a clear process for companies to become regulatory compliant and therefore be allowed to do business with banking institutions.

The country abandoned its national currency (the Zimbabwean Dollar) in 2008 in favor of the U.S. Dollar (USD) and South African Rand (ZAR), after hyperinflation reached a staggering 500 billion percent.

Zimbabwe is often cited by cryptocurrency proponents as a warning of how unchecked centralized financial systems can collapse. The nation is infamous for its outrageously high black-market Bitcoin trading prices, which has led its Reserve Bank to ban and criminalize crypto trading in 2018

The incoming regulatory sandbox aims to ascertain whether individual domestic crypto companies can be allowed to operate independently, or whether they must seek support from bigger financial partners, especially if they’re operating as micro-financing businesses.

Why it’s important

Reserve Bank of Zimbabwe (RBZ) director Josephat Mutepfa, said in a recent speech that the RBZ decided to take this forward-thinking approach as Zimbabwe’s youth are “facing challenges with having capital” and that the country needs to find a way to regulate the use of crypto.

The practice of micro-financing is a well-established business practice in Africa and vital for thousands of young entrepreneurs who would otherwise have no recourse to funding from traditional financial institutions.

According to this 2016 UN study) nearly 60% of Africans are under the age of 24 and are using their mobile phones as a substitute for bank accounts due to lack of infrastructure, risk of crime and geographical challenges. These combined reasons demonstrate why virtual assets have such a huge potential to positively impact the African economy in this new decade.

Conclusion

With the price of Bitcoin currently teetering above $5000 and the world grinding to a halt for the foreseeable future due to COVID-19, the global economy is in dire straits.

The world’ s financial systems and markets will require a long period of adjustment and recovery to which the 2008 financial crisis might ultimately pale in comparison. More economic bailouts, zero-interest rates and trillion-dollar government injections of fiat currency dollars are already in play.

It would behoove virtual asset adopters to remember the progress made this year until a force majeure stopped the world in its tracks.

Virtual assets are seen as high-risk investments due to their lack of regulations and are often the first to go when investment portfolios are subjected to financial turmoil.

These countries’ recent crypto reforms should speed up the eventual global acceptance of virtual assets such as Bitcoin and Ethereum as legitimate forms of investment and tender.

The compliance chips needed for the mass adoption of cryptocurrencies are slowly falling in place in 2020. There’s more than a sliver of hope that virtual assets will fulfill their raison d’etre and eventually provide economic sanctuary in this uncertain future.

This latest crisis is likely the moment of truth for virtual assets. While cryptocurrencies like Bitcoin have failed miserably as safe-haven assets since mid-March by ironically halving in value months before its biggest milestone of the year, so did gold, platinum, and silver.

In a financial system where the powers-that-be can change the rules as they see fit, a virtual currency like Bitcoin still offers this: a 21st-century asset class that immutably records its own history without fail, that will always remain inflation-proof due to a finite supply that can only be measured at the point where it intersects with public demand.